It’s that time of the year when graduation caps will be flung in the air and high school seniors everywhere will be reflecting on their lives as children and anticipating what they’ll do with life as a legal adult. Some will be heading off to college to tech school, while others will immerse themselves into the working world, eager to start funding their hopes and dreams.

Whatever your plans for this new era of your life, include, make sure you don’t allow money (or the lack of it) to become the stressful subject that it is for 72% of Americans. Instead, heed these 8 pieces of financial advice and start your life as an independent adult out on a path that will help ensure you never have to worry about money.

Advice for High School Seniors

When I was a kid, money was still a pretty taboo subject and people weren’t cool with sharing their money advice with “kids”. This is a big part of the reason so many adults struggle with money today.

You likely grew up in one of three types of families: One where money was always a struggle, one where money was never a struggle, or one where money was never talked about and you don’t have a clue what your parents’ financial situation(s) are.

If you’re one of the rare ones whose parents eagerly shared tips about money management and growing wealth, congratulations. Thank your parents for their wisdom, and follow their smart suggestions so you can avoid money problems for your future self and family.

If you’ve not been taught about money management or always sensed a lack of money in your family, never fear. Been there, done that, and I’m here to show you the way out of that vicious and stressful cycle.

Either way, the tips you read about here will help you improve your net worth, and if you’re smart about it, you can reach millionaire status at a relatively young age by doing what millionaires do. Get your notebooks out and be prepared to be financially savvy.

1. Accept That You Have Control Over Your Money Situation

One lesson that I got growing up (or at least that perceived growing up) was that people have no control over their money situation. I believed that it was a “luck of the draw” thing. Either you were rich, or you were poor, and whatever hand you were dealt was the hand you had to live with.

It was only after many, many money mistakes that I learned that each individual has a choice about how they earn, spend and save the money that comes to them. And I learned that income had relatively little to do with it. If income was a big factor, then 92-year-old janitor Ronald Read wouldn’t have died with an $8 million dollar estate. But he did, thanks to frugal living and regular investing.

Your money mindset will influence your level of financial stability. The sooner you accept the fact that you have a choice about what you’ll do with each dollar that enters your hands, the earlier you’ll be able to make that money work for you instead of living your life working for money. But we’ll talk more about that in section 8.

2. Learn to Get Creative About Earning Money

Gone are the days when holding a traditional job is the only way to earn cash. Luckily, you are coming into adulthood during the age of the side hustle. There are hundreds of side hustle jobs that allow you to earn money how and when you want to, and put you in control of how much money you make with them.

A side hustle can be anything from mowing lawns on the weekends deliver pizzas to selling your custom artwork to freelance writing or blogging online. Take some time to find the side hustle(s) that works best for you and use it to supplement your financial goals.

3. Make Saving a Habit

Funny thing about saving money: the earlier you make it a habit, the easier it will be to continue saving even through times of sparse income. Recently I began saving ten percent of my freelancing income. It didn’t take long at all before my savings reached 4 digits, and I only work part-time at freelancing.

Most employers and/or banks will allow you to set up an automated plan to put a certain percentage of your paycheck into a separate savings account on a regular basis. Take advantage of automating, or do it yourself, but make it a habit to save something out of every bit of income that comes into your hands?

Why?

Why is saving so important? Well, first of all, having a plush savings account buys you freedom. You won’t have to worry about making decisions about jobs or purchases based on whether or not you can afford to take a pay cut or whether or not you can afford to pay for an expense. By keeping an abundant savings balance in the bank, you can easily pay for necessities like unexpected car repair purchases or medical bills, and you can pay for treats like spontaneous trips with friends.

Second, by automating your savings you’ll build up wealth faster that you realize. Before long you’ll have $1,000 in the bank. And then $10,000. And then $50,000. And then $75,000. If you can adapt a “set it and forget it” attitude about saving a portion of each source of income, you’ll put yourself in a financial situation where you have many, many more choices than your friends who chose to blow off saving money for the “you only live once” lifestyle.

4. Buying with Cash Will Make You Spend Less

The convenience that comes with today’s plastic access to money is great. It takes away the need for people to keep track of their cash, and it helps make purchases everywhere a whole lot easier.

However, there is one glaring downside to our plastic-driven society: It takes away the value of money. Don’t believe me? Try this experiment and see for yourself. Put away your plastic and carry your money as a wad of cash in your purse or wallet.

Something interesting happens when you start paying for things with cash: you start seeing the real-life truth that you are parting with your money.

With credit and debit cards it’s just “numbers on a page”, but with cash, its’ your hard-earned money that you worked and slaved to get, and it’s going bye-bye to the cashier at McDonald’s or the ticket lady at the movie theater. Paying with cash makes it crystal clear that you are no longer as wealthy as you were five seconds ago, and it can have an impact on your spending.

Paying with cash helps you realize that when your money is gone, it’s GONE. Those numbers on paper that come from your bank are simply numbers.

5. Learn to Decipher Value Purchases vs Non-Value Purchases

If you can learn to put a value on your purchases, you’ll likely keep money waste to a minimum. The difference between value purchases and non-value purchases will be different for everyone. Each person values different things, and it’s up to you to figure out which purchases are important to you and which aren’t.

There are a few ways you can learn to decipher the difference between value purchases and non-value purchases.

Make a List of Financial Goals

Making a list of your financial goals will help you see what is truly important to you. Is your goal to pay for college in cash? To save for a new car? To save enough to purchase a house? To save enough to go to Europe with your friends?

Once you have your list of goals, you can measure up every potential purchase against those goals. When your friends say, “Hey, let’s go out to eat” you can ask yourself “What would bring more value to my life: dinner at Chili’s for the second time this week, or an extra $20 toward my new car?”

Track Your Spending

Using a spreadsheet, track every expenditure you make for 30 days. Put the expenditures into categories such as clothing, eating out, entertainment, etc. At the end of the thirty days, tally up what you spent in each category and assess the totals. Looking back, was there money spent that you now consider a waste? What would that wasted money have added up to over the course of a year?

Tracking your spending allows you to avoid having your money go into that black hole of wasteful spending where you wonder “Where does all my money go?” And in turn, it helps you to be more thoughtful about your purchases.

Equate Purchases with Working Hours

A third way you can help determine the difference between value purchases and non-value purchases is to ask yourself how many hours you would have to work to pay for an item. For the dinner at Chili’s we talked about earlier, if you make $10 a hour you’d have to work two hours to pay for that. If you wanted that cool new video game that just came out at a retail price of $100, you’d have to work ten hours to pay for that.

So the question becomes: is this purchase work ten hours of my working time? If the answer is “no” put it back on the shelf and save yourself some cash.

Understand Emotional Spending

Many, many people use spending as an emotional outlet. The book, Money Love: A Guide to Changing the Way That You Think About Money shares the story of one woman who got into – and out of – a half million dollars in debt by learning to understand how to overcome emotional spending.

If you’re finding that you spend money to gain happiness, overcome sadness or to gain acceptance, find ways to work through your emotions that don’t include spending and leave your money in the bank so it can be used to increase your financial security.

6. No Debt Means More Happiness, More Freedom

The facts are clear: debt destroys your chances for financial freedom. The media and banks tout debt as a way for you to reach your dreams, but the truth of the matter is that most times debt just forces you to live in bondage to lenders until you’ve made that last payment – IF that time ever comes.

We’ve become a society where living with large amounts of debt is “normal”. Unfortunately, stress, health problems and unmanageable payments have become normal along with it. Don’t allow yourself to be financially normal. Instead, get your financial act together now, before hundreds of thousands in debt takes over your life and ruins your dreams.

7. Learn the Value of Giving

There’s something about giving away your money that makes you appreciate it and respect it more. Giving away your money will also keep you detached from it and keep it from becoming an idol in your life. As a third bonus, giving away your money will help you have a first hand look at the people who aren’t in as good a financial situation as you are, and give you the opportunity to help them have a better life.

When deciding where to give your money, look to causes that are close to your heart. Does it hurt to hear about children in third world countries who are starving to death? Do those commercial about abandoned and neglected pets tug at your heart? Is there a ministry organization that helped you as a child that you’d like to give back to?

Make a habit of giving just as much of a priority in your life as saving is. Make helping others a part of who you are. And as a bonus, if you give to a qualified organization, you’ll reduce your taxable income and save money in the process.

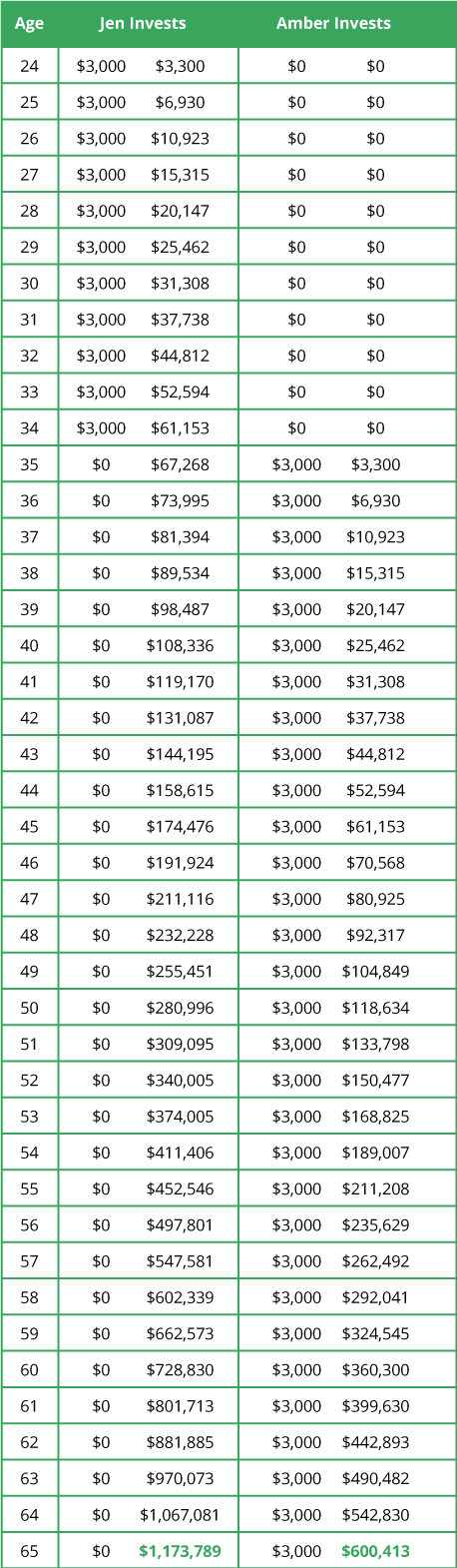

8. Take Advantage of Compound Interest

Compound interest is your enemy if you carry debt, but it’s your best friend of you use it to grow your wealth. Check out this compound interest example from www.daveramsey.com.

As you can see, Jen invested MUCH less money than Amber did as a whole. However, because Jen started so much earlier than Amber, she still ended up with nearly TWICE as much money at age 65 than Amber did.

This is the wonder of compound interest. Learn it. Save it. Live it.

9. Make a Commitment to Gain a Personal Finance Education

One of the best investments I’ve made with my time and money is to read books on personal finance and growing wealth. By educating yourself early on these two subjects, you’ll be able to avoid many of the money mistakes so many people make these days. Here are some of my personal recommendations.

The Millionaire Next Door: The Surprising Secrets of America’s Wealthy

The Legend of the Monk and the Merchant: Twelve Keys to Successful Living

Love Your Life, Not Theirs: 7 Money Habits for Living the Life You Want

Rich Habits – The Daily Success Habits of Wealthy Individuals

Buy them. Check them out from your local library. Or ask for them for graduation gifts. Just find good personal finance and wealth building books, and use your time to learn how to manage money well instead of allowing your money to manage you.

Remember: your dollars, they can be employees for you that grow your wealth. Or you can trade them in for the short-lived satisfaction of a weekly burger and fries or the latest new and shiny thing that grabs your attention.

Learn to avoid the money mistakes that so many people make, and start your adult life off with firm financial footing.

Readers, what advice do you have for high school graduates?

Great post Laurie! We’ll have to graduates in a matter of weeks. We have been invited to several graduation parties and our plan is to gift some of the books on your list. Who knows if they will get read, but I hope the will plant a seed. The advantage that every high school graduate has? Their youth and ability to learn!

So glad you are giving PF books as gifts – what a blessing it will be to those kids. I’m excited for this generation of kids. So many will choose to learn!

Great advice! Making saving a habit and tracking your spending would be at the top of my list. Too many people put off saving until they’re in a better position. You may never feel you’re in a better position — it’s all relative. And tracking is even more important than budgeting because you can make a budget and then blow it, but the numbers don’t lie when you track them.

I’ll have to check out the Legend of the Monk. I never read it.

Totally agree about saving. We thought for years that we couldn’t afford to save. Then we learned to make it a habit and found out you really can save on any budget.

I bet you’ll like the book – it’s a cool combo of fiction and personal finance advice. 🙂

This is great advice to start understanding in high school… and reminding them (and us) Every Single Year. 🙂

So true, Brad – so true!!

Great advice for the up and coming generation, hope they read the books you linked for them!

Me too. I’m making our homeschooled senior-to-be read all of them. 🙂

All of these tips are great! I really like #1 and #8 – it’s important to recognize the “choice” you have in how you use your money and that those choices can compound and completely change your life. Love this post!

Thanks, Amanda! Glad you like it! If we can help kids today avoid the same mistakes so many of us PF bloggers have made, I’ll be a happy camper. 🙂

All great tips. Wish we would have known all that back then. But even though it is a minor set back, any bad financial decisions turn into valuable life lessons. There should be a class about personal finance taught in schools. I think students would find a lot of value in it and may actually retain some of the information. Thanks for sharing.

Thanks!! I would LOVE it if more schools would get on board with PF education – and more parents. This is one of those valuable life curricula that everyone should learn about. It would save people SO much misery.

I’m thinking of the loooong list of mistakes I would have avoided had I received and followed this advice 🙂

One think I might add, if I were giving this to my own son or daughter: learn to control your impulses. A solid foundation is easily wiped out in a moment of weakness.

That’s another good one, Ty. Appreciate the input!

Love this! Now to find a graduate to share them with!

It’s so much better to learn from others than to make your own mistakes.

SO true!

Ugh I vividly remember the moment I first saw that compound interest chart…. when I was 38, with maybe $5000 in retirement investments :/

I love all these points. My son is already a bajillion times more financially savvy than I was, for which I am immensely grateful. And I keep forgetting to add The Legend of the Monk and the Merchant to my reading list, so thank you for the reminder!

That is so awesome that your son is making smart financial moves, Kat. You’ll love the Legend of the Monk and the Merchant – it’s a great read!

Saving money has to be a consistent habit. I had been trying to save in bits ever since I attended my first summer job. I started paying for my insurance soon after. Thanks to my parents for making me responsible. But then, I still make a consistent effort to find out more ways that allow me to save. Managing your finances gets easier when you stick to your budget and use your cards responsibly!

“The Wealthy Barber” talks about the importance of a consistent savings habit. You’re lucky your parents taught you the importance of financial responsibility. It makes a difference! Thanks for weighing in – we appreciate it!

Good post! I liked hearing that story about the janitor, although I don’t know if there was any proof he amassed that fortune on his own (he could’ve inherited at least a portion of it).

On #7, if you’re interested in giving away your money, I’d recommend checking out GiveWell, a non-profit started by two former hedge fund managers, that examines the efficacy and current funding of other non-profits, so you get the best bang for your buck.

The sad part is there is, unfortunately, a lot of fraud in the non-profit sector. It isn’t really that easy to guarantee your money is going where you want it. I’d also recommend reviewing the charity on Charity Navigator before giving it away.

Then again, don’t overthink it. Something’s better than nothing.

We’ve used Charity Navigator before: it’s a good resource. Thanks for your comment, Phil!

Hi Laurie,

That is a great list for high school students. The sooner they learn these lessons the better off they will be in the future. There might not be too young when it comes to learning about personal finance.

Thanks, Dave!! We have one high schooler and three more that will be there soon enough, and I SO want them to avoid the financial mistakes we have made.